In July 2023, the Department of Education announced a new repayment plan called Saving on a Valuable Education. The plan has the most generous monthly payment formulas and prevents unpaid interest accumulation, but could result in higher payments or unintended consequences for some borrowers. Read through this page for our full analysis.

Pros & cons

SAVE results in lower monthly payments for most borrowers because the protected income threshold is higher. Under SAVE, the amount of income that is protected from consideration is 225% of the federal poverty standard, versus 150% for IBR and PAYE and 100% for ICR.

Under SAVE, borrowers will not have unpaid interest accrue. If you make your monthly payment, your loan balance won’t grow due to unpaid interest. Borrowers in this new plan will no longer see their loans growing over time, reducing the risk of IDR, PSLF, and public service or lower-paying careers.

Some of the existing IDR plans have limited interest subsidies. For instance, under PAYE and IBR, the Department of Education subsidizes unpaid interest for the first 3 years of plan enrollment for subsidized loans. But under SAVE, this benefit lasts throughout the life of your loan and for all loan types.

If you switch to SAVE and already have unpaid interest on your loans, that interest will not disappear. It’ll either continue being unpaid interest, or, if you’re switching to SAVE from the IBR plan, it’ll capitalize and be added to your principal balance.

Under SAVE, married borrowers will be able to file taxes separately to have the borrower’s sole income determine their monthly payment amount. This is a change from the existing REPAYE plan, where combined income is considered no matter a borrower’s tax filing status.

Under new regulations, a borrower who files taxes separately will no longer have their family size include their spouse. According to these new rules, some married borrowers could see their monthly payment increase.

IBR and PAYE require a “partial financial hardship,” which is a function of a borrower’s debt-to-income ratio. The partial financial hardship requirement puts a cap on your monthly payments under IBR and PAYE. Under those plans, your monthly payment can never be higher than the Standard 10-year repayment plan amount. If your debt-to-income ratio reaches those levels, you’ll be removed from IBR / PAYE and put back into the Standard plan.

SAVE does not have a monthly payment cap. That means that your payment could rise above the Standard 10-year plan amount if your income is high and your loan debt is low. For some borrowers, SAVE could result in higher monthly payments than the Standard 10-year plan. If this happens to you, you can always revert back to the Standard plan.

Most of the benefits of the SAVE plan apply to graduate and undergraduate loans alike. However, there are a few key differences.

Borrowers with undergraduate loans will see their monthly payments reduced even further starting in July 2024. Under SAVE, borrowers with undergraduate loans will pay only 5% of their discretionary income toward their loans each month. Borrowers with graduate loans will pay 10%. Borrowers with a combination of undergraduate and graduate loans will pay according to a weighted average rate. Compare this with the 10% borrowers pay under PAYE, the 10-15% borrowers pay under IBR, and the 20% borrowers pay under ICR.

If a borrower is seeking forgiveness under an IDR plan (as opposed to 10-year PSLF or paying off their loans), it will take 20-25 years under the new SAVE plan. Borrowers with undergraduate loans can get their loans forgiven after 20 years of making payments in the SAVE plan. Borrowers with graduate loans will need to make 25 years of payments.

Compare this with the across-the-board 20 years to forgiveness under PAYE. IBR, REPAYE, and ICR all require 25 years. This means that PAYE could be a better option for someone who intends to take advantage of IDR forgiveness after 20 years.

Borrowers with low loan balances can see forgiveness before 20-25 years under SAVE. Low-balance borrowers can see forgiveness in as few as 10 years if their original principal balance was less than $12,000 Each $1,000 borrowed above $12,000 adds one year to repayment until borrowers reach the 20 or 25-year cap. If you have a very low original loan balance, SAVE could be the better plan for you. As of January 2024, the Department of Education has started forgiving borrowers’ loans who are enrolled in the SAVE plan and meet these qualifications. *This provision of SAVE is on hold pending court decisions.

SAVE does not have any eligibility limitations. Borrowers with graduate or undergraduate, and subsidized or unsubsidized loans can join. New and older borrowers can join, and borrowers with any income can join.

If you switch to SAVE, you’ll need to provide your latest income information. This could change your monthly payment earlier than your existing IDR plan’s expiration date.

If you’re currently in the IBR (Income-Based Repayment) plan, switching to SAVE will have some consequences. First, you’ll need to elect to pay a one-time $5 monthly payment during the switch, which won’t count toward PSLF. Any unpaid interest will also capitalize, or getting added to your principal balance.

What should you do?

Whether the SAVE plan is better than the existing IDR plans will be a different question for each borrower. Consider some of these questions:

- What’s your long-term loan repayment strategy?

- If you’re pursuing PSLF, it might not matter to you how much interest accrues over the life of your loan.

- If you’re planning to pay off your loan, it matters a whole lot more how much interest accrues.

- If you’re hoping to pursue 20-25 year IDR forgiveness, it does matter how much interest accrues (because the amount forgiven will be considered taxable income) and how long it takes to get forgiveness.

- Are you married, and how do you file taxes?

- If you file jointly, take a look at your combined income and see which plan results in the lowest monthly payment.

- What plan are you in now?

- If you’re in PAYE, you have the option of switching. PAYE will sunset July 1, 2024–if you are not enrolled in PAYE at that date, you will not be able to re-enroll. If you want to switch to SAVE, your unpaid interest will not capitalize.

- If you’re in ICR, you have the option of switching. ICR will sunset July 1, 2024–if you are not enrolled in ICR at that date, you will not be able to re-enroll. If you want to switch to SAVE, your unpaid interest will not capitalize.

- If you’re in IBR, you have the option of switching. IBR will not sunset, so new and existing borrowers will be able to enroll in IBR. If you want to switch to SAVE from IBR, any unpaid interest will capitalize and be added to your principal balance.

Most borrowers haven’t updated their IDR income since before the COVID payment pause. That means the income your current IDR plan is based on could be from 2019 or 2020. If your income has increased since you last applied for IDR, you may see your monthly payment increase if you switch to SAVE right now, even though SAVE uses a more generous formula. That’s because when you switch plans, you’re required to update your income.

For many borrowers, it probably makes sense to wait until your current IDR plan expires to switch to SAVE. Use this time to consider whether switching makes sense for you. To view your current IDR plan details:

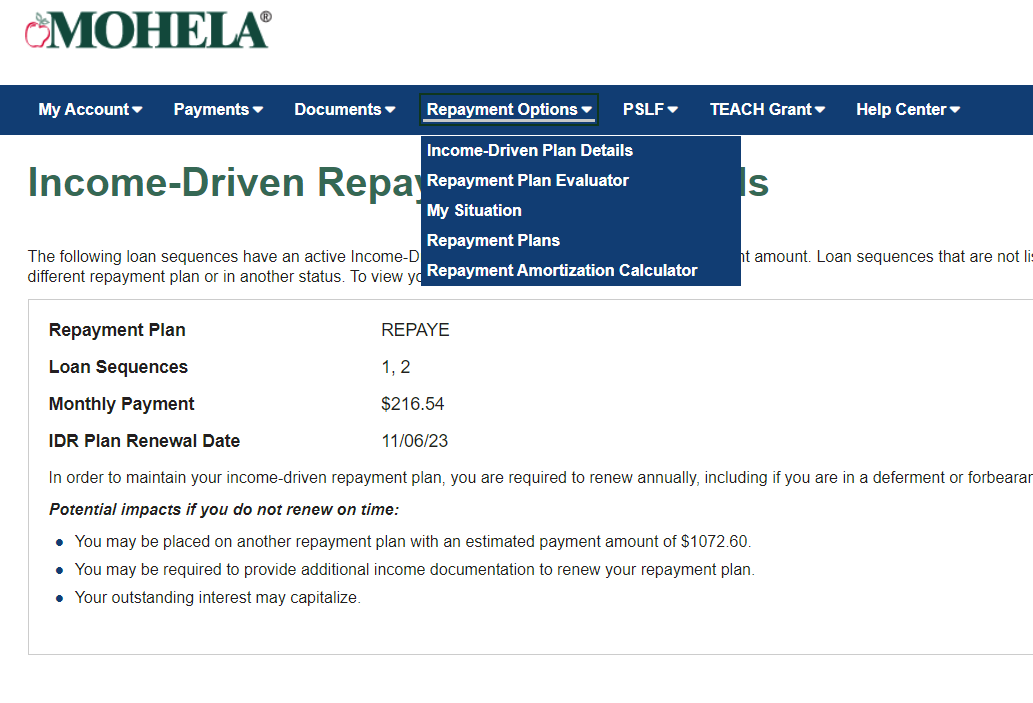

- If MOHELA is your servicer, log in and go to the Repayment Options → Income-Driven Plan Details page. View an example.

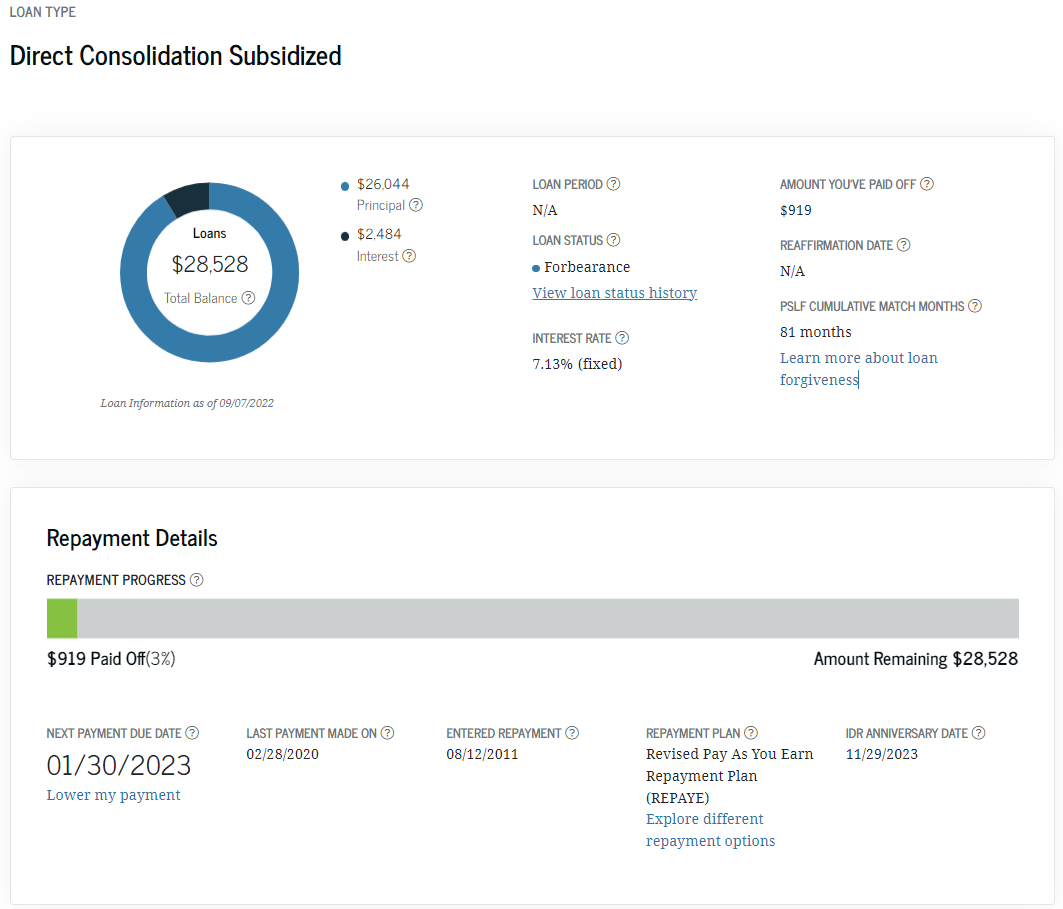

- Log into studentaid.gov. In the My Aid dashboard, click View Details. On your Loans page, click View Breakdown and then the View Loans down arrow for your DEPT OF ED loans. Click View Loan Details for any one of your loans. Scroll down to the Repayment Details box and look for an IDR ANNIVERSARY DATE. View an example.

{kind=link}

{kind=link}

Last updated July 15, 2024