{kind=link}

{kind=link}

COVID payment pause

Interest on federal student loans resumed accrual in September and payments are resuming in October.

To prepare for the resumption of payments, follow these steps:

- Log into studentaid.gov to check who your loan servicer is. While you’re there, update your contact information.

- Set up an online account with your loan servicer and enroll or reauthorize auto-debt. Update your contact information, make sure you’ve specified whether you want mailed or paperless communications, and enroll in auto-debt to receive an interest rate deduction and ensure you’re making on-time payments. Because most of us have switched loan servicers since payments were last due, your new servicer may not have your bank account information, so you’ll need to provide that info and enroll in auto-pay.

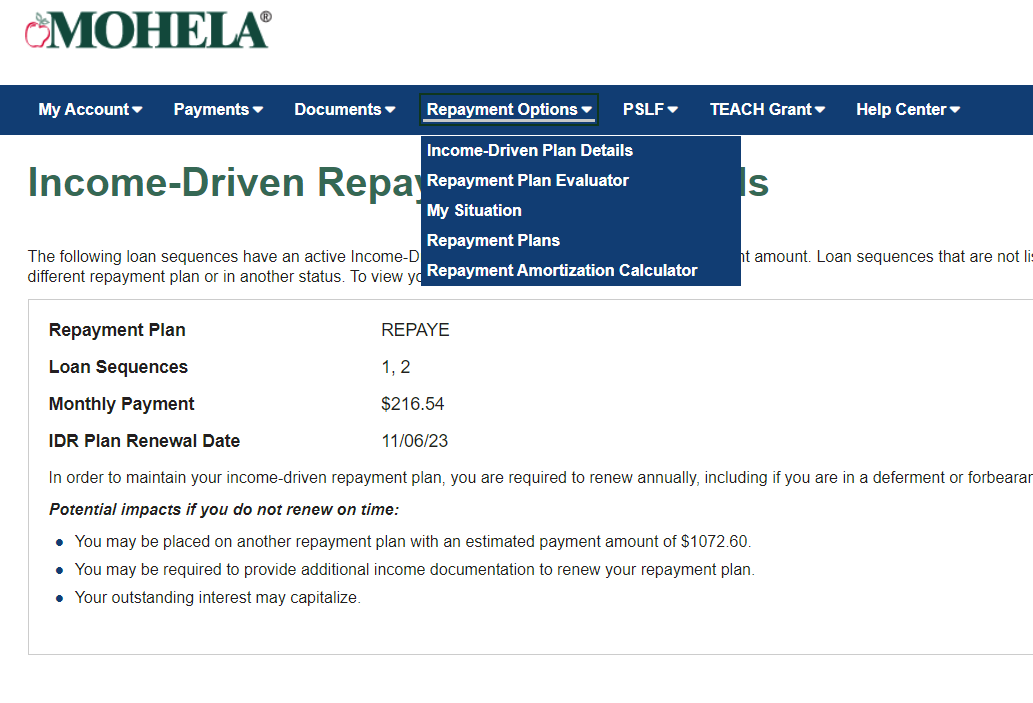

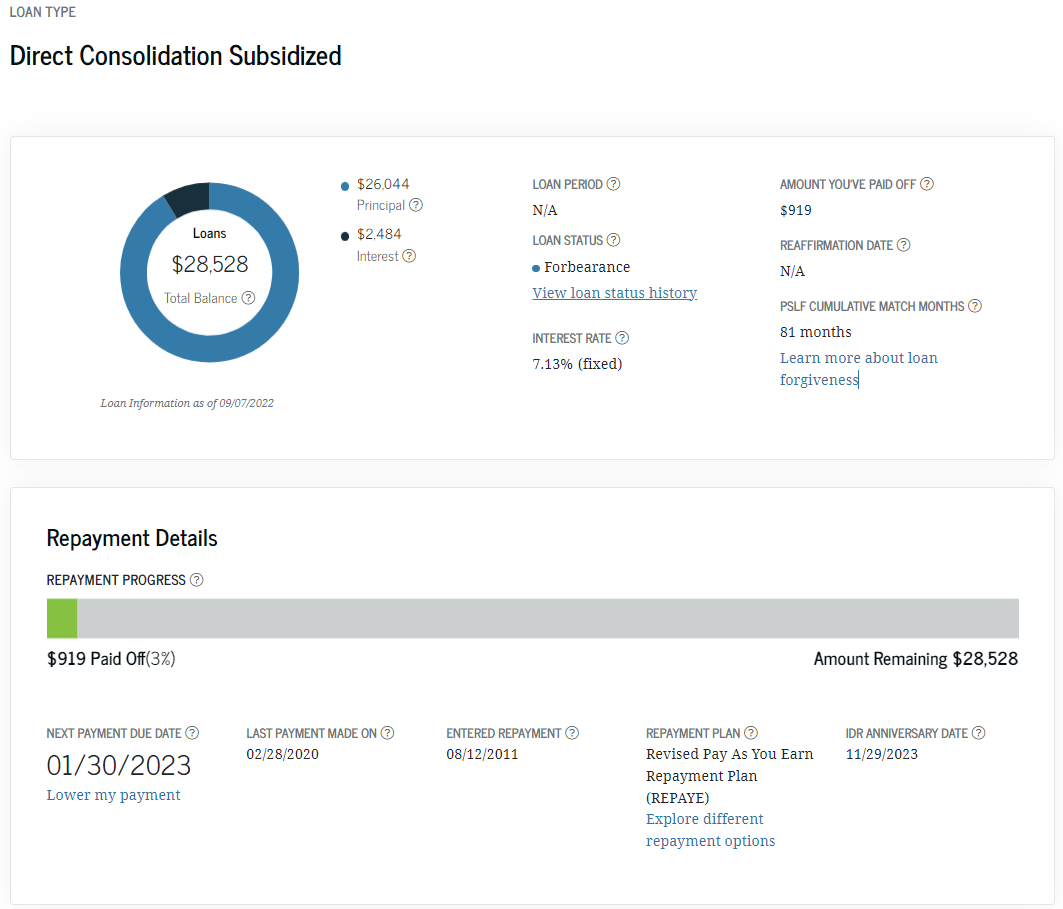

- Review your monthly payment and payment plan. What will you be paying, and when is your payment due? What repayment plan are you in, and is the plan still working for you? If you’re pursuing Public Service Loan Forgiveness(opens in a new tab), you’ll want to be in an Income-Driven Repayment plan(opens in a new tab). If you recently submitted an IDR application or switched loan servicers, that information may still be pending.

- Make sure you’re taking action early and not waiting until the last minute. You could miss a payment or end up in an unaffordable payment plan.

- Review your budget and prepare for an increase in expenses.

- Getting ahold of your loan servicer can be challenging right now. Be patient; you may need to call multiple times or use the live chat or email feature. If you need to get ahold of your servicer, set aside some time to account for long holds.

- Keep documentation of your payment plan, payments, PSLF and IDR applications, and correspondence with your servicer.

- Problems with your account? Contact your servicer and the regulators. Borrowers have been having trouble with their servicers, sometimes getting kicked out of their IDR plan, having their monthly payment miscalculated, or not receiving a billing statement. To find a resolution, you can file a complaint with the California Department of Financial Protection and Innovation and/or contact your loan servicer.

Miscellaneous updates

There has been in increase in student loan scams since the COVID-19 and student loan relief announcements. Be aware of scammers and know that the federal government will never call to ask for a fee to suspend your loan payments. Report any scams to the FTC or the California Department of Financial Protection and Innovation.

last updated March 1, 2024